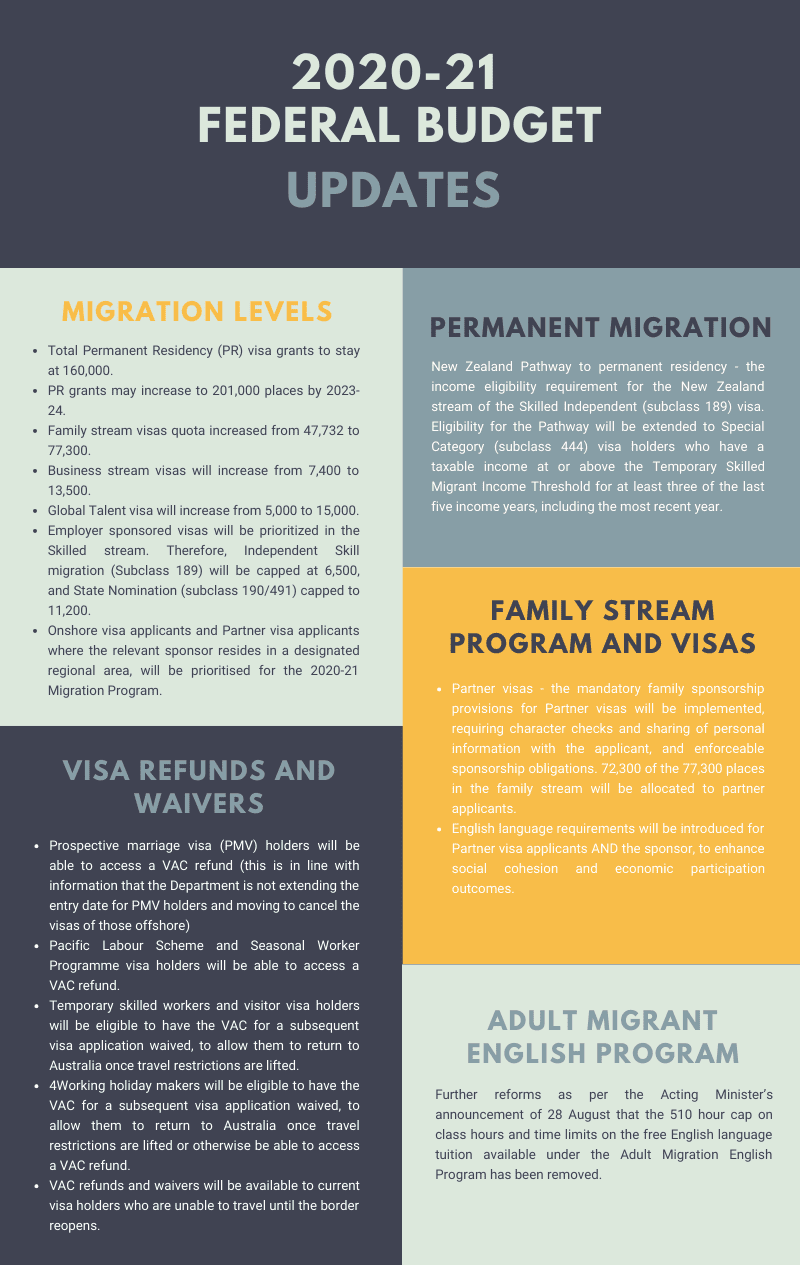

Can Property Investment be an “Eligible Business” for Business Visa in Australia?

I am often asked by new and perspective business migrants on whether they can invest in property for the purpose of satisfying the Australian Business Visa requirements. The good news is that it is possible. Investment in property may [emphasized] meet the migration requirements.

I must emphasize 2 important points: (1) Passive investment (and more specifically, provision of rental properties to the public) and smaller “project” based property development will NOT meet the migration requirements; and (2) Even if the migrant’s proposed business in property investment meets the State’s guidelines in bringing in substantial and exceptional benefits and thus obtained nomination by the State or Territory, this itself does NOT automatically mean that the Commonwealth migration requirements are met.

Under the Commonwealth migration regulations, a business migrant must satisfy three (3) conditions under the Act: (1) The business proposed or carried on by the migrant must be an “eligible business”; (2) The migrant must have obtained a substantial ownership interest in the eligible business; and (3) The migrant must actively participate at a senior level in the day-to-day management of the eligible business. If the migrant fails to satisfy these requirements, the Minister may cancel the visa. Hence, business migrant, please BEWARE!

This article briefly examines the “eligible business” requirement. In the case of Zhonghua v Minister for Immigration and Citizenship (BC201102754), the migrant, holder of sub-class 132 Business Talent visa, invested AUD$3,000,000 into a property development project. There were submissions by the migrant that application to re-zone the property was made to develop apartments. However, the Tribunal found that the investment did not pass the initial stage of purchasing the land. No actual development has taken place other than owning the land and making application to re-zone the land. For this reason, it cannot be described as a business. As such, the migrant’s investment did not satisfy the “eligible business” definition. However, what is important from this case is that in the judgment, the following comment was made by the presiding Senior Member, Mr Egon Fice: “… if the development proceeds, it might satisfy the eligible business definition in that it might create or maintain employment in Australia or result in commercial activity and competitiveness within sectors of the Australian economy.”

Further, under the case law, the test of what constitutes an “eligible business” requires more than just satisfying the conditions under the migration regulations. The Courts require that the business has repetitiveness of activities and some permanence characteristics: Puzey v Commissioner of Taxation [2003] FCAFC 197.

For the professionals who assist business migrants with their investment (such as migration agent, accountant, and real estate agent), you should find this article beneficial or at least relevant. Australian Courts have strict expectations that the requisite standard of care is met and professionals could be found personally liable for negligence or wrongdoing if the standard is not met. Here is a thought: What do you need to do (or must not omit to do), in order to meet the requisite standard of care?

For businesses seeking investment capital from the business migrant (for instance, property development company), beware of “representations” (such as statements and forecasts) that you make to the investor, buyer or migrant. If your representations are subsequently found to be false, even if it was not your intention to lie, you can be liable for damages for having engaged in “misleading or deceptive conduct” under the Consumer Act. This is a huge exposure to liability.

There are also cases where migrants have failed the “substantial ownership” requirement due to technical difference between legal ownership interest and beneficial interest. The ownership structure of the project company is extremely important. My next article will examine the ownership issue in more details.

Writer:

KELVIN TANG is the Principal Partner of Tang Law. His areas of practice include Investment Law, Commercial and Corporate Law, Property Law and Immigration Law. Relevant to this article, his expertise, knowledge and experience include representing property developers and new migrants with acquisition of property, structuring of investment vehicle, joint venture transaction, and advice on commercial transactions.

Telephone: +618 9328 7525